An introduction to where market price data comes from and how you can use it to objectively assess your clean energy project options.

Markets

5 minutes

Introduction to different commercial structures in energy projects

The physical attributes of energy projects can be complex - asset sizing, control strategy, weather, grid constraints, loss factors and asset degradation to name a few considerations - but when you add in the commercial side then things get even more interesting. At the end of the day a solid commercial business case is required to get a project off the ground, and understanding how these projects make money, and for who, is critical.

In this article we explore a few common commercial structures in energy projects and delve into the impacts of who pays for what, how they get paid and how those commercial arrangements may impact the physical project design decisions, including optimisation approach, … and outline how all of this can be modelled in Gridcog.

Buying and selling energy

There are a myriad of different commercial constructs that can be used in energy projects to represent the relationship between the buyer and the seller of energy and/or to help hedge, finance or de-risk parts of the project.

Power Purchase Agreements (PPAs):

Put simply, PPAs represent the way you sell the power that you produce. In Gridcog, assets that can earn PPAs are renewable generators such as wind and solar sites and Generators sell the power they produce via a number of different structures.

PPAs can be purely financial or linked to physical energy flows. A physical PPA can either be a private wire arrangement, which could be based on consumption or total generation, or they can be market facing, for example where the PPA offtaker registers your MPAN/NMI/meter and pays you for every MWh of energy that is exported through it.

Physical PPA prices are usually fixed across different time periods (e.g. summer/winter), may be referenced to a certain market index (e.g. N2EX Day Ahead) or be priced across a combination of these markets. Usually PPAs will include a fixed or passthrough element for non-power benefits including green certificates, subsidy schemes and embedded benefits.

PPA offtakers can vary quite considerably but may include retailers, suppliers, aggregators or landlords in private wire arrangements. If you’re interested in learning more about PPAs we’ve included a deeper look into some common PPA structures at the bottom of this article.

Supply Agreements/Retail Tariffs:

These are arrangements for the purchase of electricity from your Supplier or Retailer. Like PPAs they will usually include a fixed or floating price represented in $ or £/MWh for the power you consume - this price is likely to vary depending on the time of day that you consume power, known as a Time of Use (TOU) tariff structure. Retail tariffs are likely to include non-commodity charges as well, these will be represented as a fixed or percentage passthrough cost, if they are a passthrough your bill will likely include an estimate of what they will be. Non-commodity charges include things like Standing charges, RO/CfD, RCRC, BSuOS.

Optimisation Agreements:

Flexible generation assets, such as batteries, gas peakers, flexible plant or electric vehicle fleets enabled for vehicle-to-grid (V2G) will likely be contracted via optimisation agreements rather than PPAs or Supply Arrangements. We’re also starting to see renewable assets enter into optimisation agreements alongside their PPAs, usually with the same party; this is to manage their participation in balancing or curtailment markets.

Optimisation agreements are common commercial structures for flexible assets because a flat £ or $/MWh rate is unlikely to represent the most optimal value from the flexibility these assets can provide. Normally optimisation agreements are structured as a revenue share (also known as merchant structure) whereby an optimiser or flexibility provider takes a certain percentage of all profits earned for providing market access and trading services; this is useful as it keeps the incentives of the flexibility provider and asset owner aligned.

In some cases, particularly for large assets, floors or tolls may be contracted instead of a revenue share arrangement. These are where the flexibility provider provides some guarantee of revenue (normally annualised) in exchange for a higher upside above the guaranteed level; these structures can be useful for people pursuing specific financing arrangements for their assets.

Financing energy assets

Most commonly one party (i.e. the Developer/Customer) will be financing the energy assets and covering their capex costs. However, increasingly we are seeing more hybrid financing models arise; these include lease arrangements between suppliers and customers, landlords financing PV systems and selling excess generation to tenants, community battery projects and rent-a-roof solar systems. In these scenarios the capex cost could be spread across multiple parties or one party could be seeking to recover their investment via a PPA, Lease or Optimisation Agreement.

Additionally, some Gridcog clients model cashflows for financiers and investors who are providing financing to allow them to invest in energy projects. Understanding these cash flows and how they change over time can be vital when building an investment case.

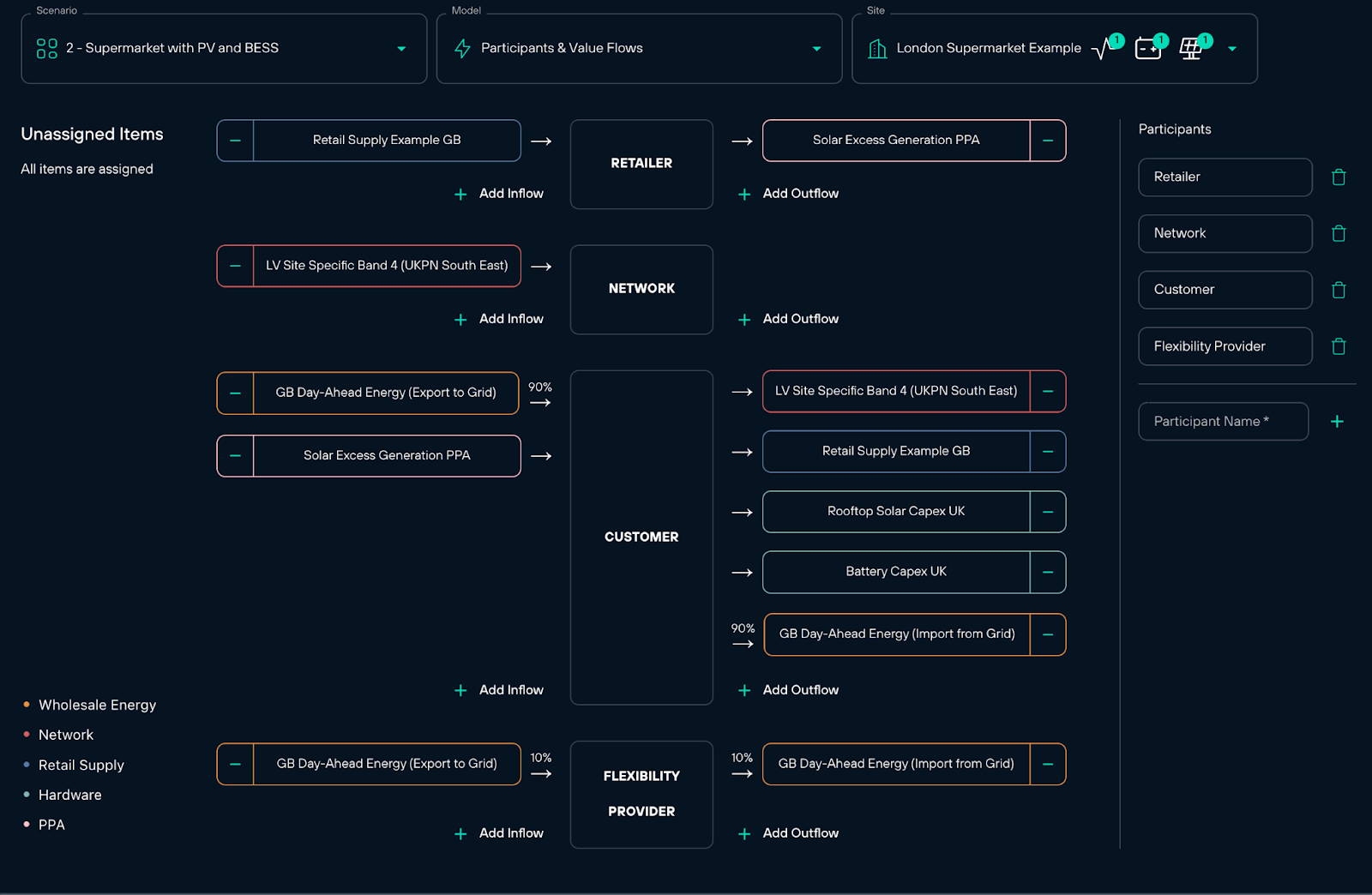

Representing all of this in Gridcog

To reflect different commercial arrangements in Gridcog we’ve developed what we call a ‘Participants and Value Flows’ model. Here you can first define the project participants you’d like to model cashflow positions for and then assign financial inflows and outflows to each party. You can even run multiple scenarios testing different commercial structures. This allows you to work out who is ‘winning’ in different scenarios and ultimately whether the project lines up economically.

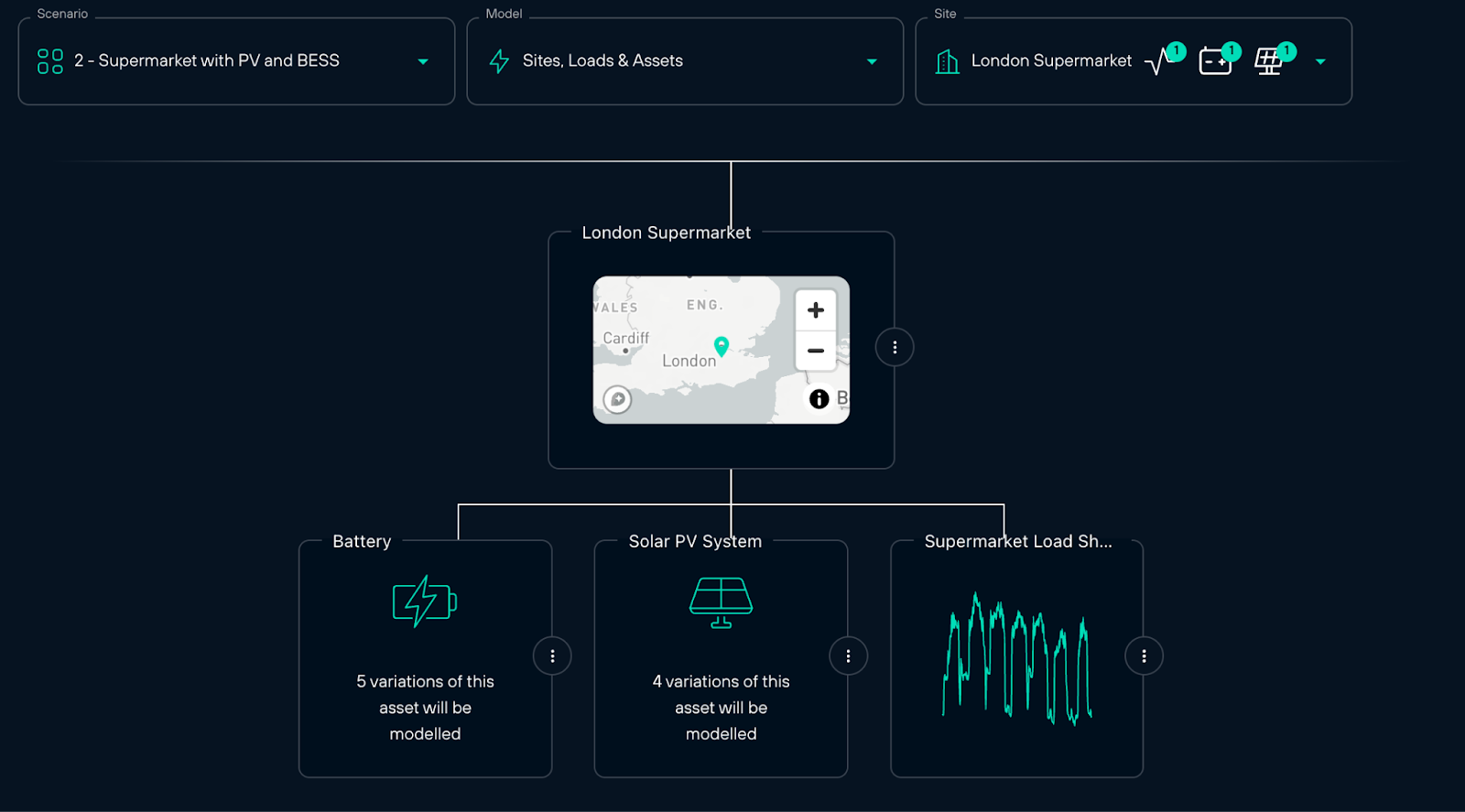

Below we’ve included a few screengrabs of the Gridcog user interface where we are modelling the commercial value flows for an example London supermarket exploring adding different sizes of battery storage and solar PV in a behind the meter co-optimisation arrangement. In this example the supermarket owner is directly exposed to the wholesale market.

There are four participants that we have modelled value flows for in the project:

- The energy supplier (retailer)

- The flexibility provider

- The supermarket (customer)

- The network operator

All of these parties are either buying, selling or financing the energy project and we’ve shown how Gridcog allows you to attribute the relevant value flows to each one.

Optimising for different participants:

Finally, the vested commercial positions of different participants in energy projects will invariably drive asset optimisation behaviour.

Gridcog allows you to optimise steerable/flexible assets for different parties - this might just be the customer or the optimiser whereby our optimiser will work to drive the highest returns for those parties.

Looking at the previous example, the network did not have a vested position in the energy project, so the steerale assets in that project (the battery) would look to make money from avoiding importing in DuoS red band periods and likely discharge into them as well, reducing earnings for the network (although also hopefully reducing their operating costs if those tariffs are vaguely cost reflective).

Learn more:

If you’re interested in learning more about how Gridcog can model different commercial structures contact us for a demo.

Additional PPA structure information:

PPAs broadly fall into a few different categories, which we will explore below:

- Private wire or behind-the-meter PPAs: These are where energy is sold between one party and another before that energy is exported to the grid (i.e. the power does not flow through the boundary meter/MPAN/NMI). An example of a private wire PPA is a landlord who has solar PV on the roof selling some of the output of that PV to their tenants. These PPAs will normally have a fixed price $/£/MWh, which may vary depending on the season/year and will likely be either generation based or consumption based.

- Physical/merchant PPAs: These are energy sale agreements associated with the physical flow of power out of the meter, they are usually as produced which means all of the energy generated is sold at the agreed price. The agreed prices can be fixed, seasonal, may have shaped rates and can also be the passthrough of certain markets or indices i.e. Day Ahead or System Price or may even be a combination of a few of these price points (block and index); the most common structures are fixed or index price PPAs. The site design and size of renewable assets will likely determine the type of PPA and any additional contractual or volumetric conditions that may be associated with it.

- Virtual/financial/corporate PPAs: These are PPAs that are usually financially rather than physically settled, this means that the counterpart may not be a supplier and will not register the meter. These structures are typically used for financing and hedging and are usually for longer tenors than physical PPAs. The shapes of these PPAs may also be baseload or referenced to a baseload price rather than the forecast or actual generation shape and may not be for 100% of the volume that the generation asset would expect to produce.

- General: Usually physical PPAs will include pricing for green certificates (i.e. REGOs/LGCs/GOOs), embedded benefits, subsidies and balancing risk (delta between forecast and delivered MWh) and supplier margin deductions. These rates can be fixed or passthrough depending on commercial arrangements.

Genna Boyle

August 25, 2023