Here’s a quick video building on our recent blog post on community battery network tariffs.

Community Batteries

11 min read

Network pricing signals for community batteries. Which network offers the best tariff?

Overview

This post was edited on 9 September 2022 to correct the results for the Evoenergy Residential Area tariff

The energy system is in transition. We’re shifting away from a small number of large centrally located and primarily thermal (fossil-fuel powered) generators to a very large number of small, distributed and primarily renewable (wind, solar) generators and energy storage systems (batteries).

As an industry we’re still experimenting with deployment models, ownership models, and commercial arrangements for these new resources. One area of strong interest is community batteries.

These are medium-sized batteries connected directly to the distribution network, without any co-located load or generation, that should be delivering value to local customers (the ‘community’ in ‘community battery’).

Australia is seeing the first waves of these batteries being deployed, and in early 2022 the Australian Energy Regulator (AER) approved a number of distribution network trial tariffs in the National Electricity Market (NEM).

These new tariffs are explicitly designed to enable these standalone batteries. Eight distribution networks have developed tariffs: the Victorian networks Powercor, Citipower and United Energy (these distributors have the same parent company); in New South Wales Ausgrid and Essential Energy; and in the ACT Evoenergy.

These tariffs all have similar objectives and are all trying to signal a certain behaviour: charging from the grid in the middle of the day when solar is plentiful and discharging back into the grid in the late afternoon when demand is highest. But these tariffs have very different designs, which we’ve summarised below.

Ausgrid Community Battery Tariff (EA962/963)

The Ausgrid tariff is primarily based around pre-defined peak demand and export events – not dissimilar to AusNet critical peak events. At this stage Ausgrid has not provided further guidance on the timing or trigger of these windows, so we’ve assumed they correlate closely with NSW total system peaks.

Powercor/CitiPower/United Energy Distributor Owned Community Battery Tariff

The same tariff structure is shared across Powercor, Citipower and United Energy. This tariff eschews all complex demand elements and is an extremely simple time of use volumetric energy tariff with a low fixed supply charge.

One important note is that this tariff is limited to a maximum battery size of 240 kVA.

Essential Energy Bi-directional Distribution Support Tariff

Essential Energy has implemented a fairly complex time of use tariff based around a core sun soaker window which encourages the battery to charge and has steep charges to discourage discharging to the grid.

Western Power, who operate the South-West Interconnected System (SWIS), in Western Australia’s Wholesale Energy Market (WEM) has a very similar trial tariff, which we might look at separately in some WEM focused analysis.

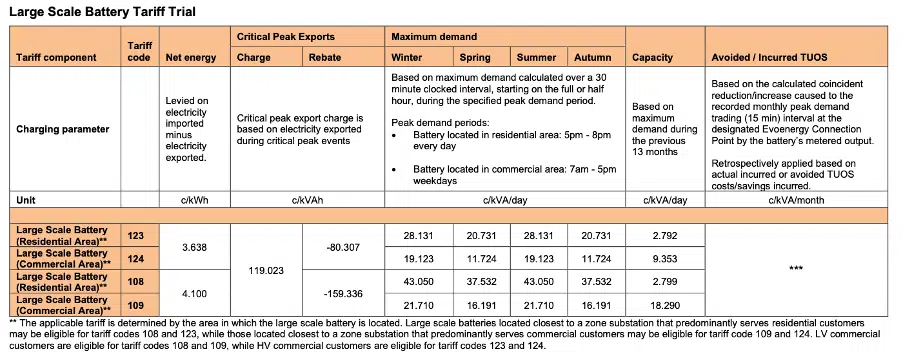

Evoenergy Large-Scale Battery Tariff

However we’ve saved the best for last. Evoenergy have implemented every type of tariff structure seen above – they’ve combined volumetric energy charges with demand charges, a rolling peak demand charge and export events like the Ausgrid tariff.

To make things even more complex the pricing varies not just by location of the battery, but also based on whether the connection is LV or HV, and the specific connection point (which determines TUOS charges).

In configuring this tariff we’ve assumed that the full benefit of the TUOS savings will be passed on to the battery and we’ve chosen a TUOS that’s the average of the ACT connection points. We’ve also only modelled the LV tariffs (108 and 109) to be consistent with the other tariffs.

These tariffs are limited to a minimum battery size of 200 kVA.

Modelling time

To understand these tariffs better, we’ve fired up Gridcog to simulate how a theoretical battery would respond to these different structures and prices, and to forecast the commercial returns that could be expected based on the assumption that the primary reason folks will invest in these batteries is to provide market services; so wholesale energy arbitrage and contingency frequency control support.

For now we’re focused on understanding the impact of tariff design and network pricing, so we’ve made other aspects of the modelling consistent to make comparison easier.

Specifically, we’ve made the following assumptions across all batteries:

- A 1 MWh, 1 hour duration battery (Note that the Powercor/Citipower/UE tariffs are limited to batteries smaller than 240 kVA, and the Evoenergy tariffs are restricted to a minimum of 200 kVA)

- All batteries have been priced against the same NSW market pricing curve to enable a fair comparison. This is just the last 12-months of pricing cast forward with introduced uncertainty, so the financial results will be quite generous.

- Two scenarios were compared – wholesale energy alone, and wholesale energy plus all six contingency FCAS markets.

- There is no co-located load or generation

- We’ve not included any capex, opex or other grid augmentation or balance-of-plant costs

The results

The overall commercial returns are broadly similar, but there’s a lot of ‘devil in the detail’.

The charts below show revenues for 10 years. The orange bars are the net wholesale energy revenues and the red bars are the net network revenues (or costs). The purple bars are the revenues from the six contingency FCAS markets. The grey bars represent upper and lower bound uncertainty due to forecasting challenges.

Wholesale energy only results

Wholesale plus contingency FCAS results

Here are some observations:

- All of the tariffs are a net cost on the operation of the battery, except for the Essential Energy tariff – the battery is able to charge for free during the middle of each day and has a generous (10.8 c/kWh) rebate for evening exports which offsets these charging costs.

- Despite very different tariff structures wholesale arbitrage values are remarkably similar across the tariff designs, excepting the Evoenergy comercial area tariff. The very high capacity charge of this tariff limits the opportunities for when the battery can efficiently charge from the grid

- Contingency FCAS revenues are a healthy revenue stream for all of these batteries – as a reminder batteries participate in contingency FCAS by maintaining state of charge and receiving payments for being on standby.

Now here’s where things get interesting: whilst the revenue opportunities are quite similar, the battery behaviours required to achieve these are not. As an example, the following load traces are taken from the second week of February – away from peak event windows and extreme market volatility.

The purple line is the battery state of charge and the blue line is the grid import/export – exports to the grid are negative.

Ausgrid battery

In a standard week, away from the defined peak energy events, the battery charges slowly during the day (when it’s charged at 1.6c/kWh) and receives its primary revenue stream by discharging aggressively into the evening peak (where the intraday spread is sufficient).

This slow rate of charging is due to the battery minimising imports from the grid to avoid the high capacity charge of $1.72/kW/month; in the load trace above the battery draws a maximum of 73 kW from the grid.

Essential Energy battery

The battery is almost metronomic in its consistency, due to the structured nature of the sun soaker window and evening rebate. The battery charges at the beginning of the sun soaker window every day, and fully discharges into the evening rebate period. The wholesale revenue is mostly a result of the difference between the prices during these two periods.

Powercor/Citipower/United Energy battery

The Victorian battery has a profile similar to the Essential Energy battery, but because of the lower charging and discharging network charges it chases wholesale energy arbitrage more aggressively – the volumetric energy charges are low enough that it is beneficial to cycle multiple times a day.

Evoenergy battery (Commercial Area Tariff)

You might be looking at the above load trace and thinking something is wrong with the battery… but this is a logical outcome of the very high capacity charge imposed by Evoenergy – the battery charges very slowly and only discharges when there’s an intraday wholesale pricing spread sufficient to overcome these high charges. This lack of cycling also results in much lower wholesale revenue streams compared to the other network tariffs (but also much lower battery degradation).

Evoenergy battery (Residential Area Tariff)

The version of the battery tariff for assets located in primarily residential areas yields better results. This tariff has a capacity charge which is an order of magnitude lower than that of batteries located in commercial areas. This leads to a lower intraday pricing spread required to overcome this charge. This tariff has a demand charge in the peak evening comparable to the Essential tariff, but without the ability to charge for free during the day. Add in the daily capacity charge which still applies to all charging from the grid and the battery doesn’t cycle anywhere near as much as the Essential battery does.

Final Observations

What’s fascinating is that four very different network tariff structures produce results that are surprisingly similar, but the battery behaviours required to achieve these outcomes are very different.

These different battery behaviours have real world implications – higher levels of cycling will affect battery performance over its lifetime, although it seems unlikely that the reduced cycling of the battery on the Evoenergy commercial area tariff could make up for its significantly reduced revenue relative to the other tariffs. The trade off is more likely to be between the daily cycling of the Essential Energy tariff (and the highest revenue) and the more conservative Ausgrid profile.

These community batteries should be deployed with sophisticated real time control systems (optimisers) that are able to correctly account for the network charges and manage wholesale energy arbitrage and FCAS participation.

But some of these tariff designs are remarkably creative and complex! There’s no point having a price signal that customers and assets can’t respond to. We are a small part of a global ecosystem and the vendors selling battery optimisers aren’t necessarily going to want to test and tune their software for exotic tariff designs. It’s interesting to note that the very simple time-of-use volumetric energy tariff of the Victorian distributors seems to be pretty effective.

This is a subject for another day, but we would love to see the Australian distributors becoming less creative, or at least a bit more consistent, and starting to adopt more evidence-based pricing models, rather than the current ‘choose-your-adventure’ we have in Australia, where every DNSP is different, and which has created whole cottage industries of tariff and billing validation and network tariff optimisation services.

One last word of caution – this analysis was done using the last 12-months of energy pricing, and the last 12-months have certainly been interesting. Different forward price curves will deliver different results, and depending on real-world project costs and O&M costs, and with more conservative market pricing assumptions, we wouldn’t necessarily expect all of these batteries to be profitable!

So what does this kind of analysis mean for you? If you are a community energy supplier or infrastructure investor interested in owning and operating a distribution-connected batteries, then modelling like this can help firm up revenue forecasts and support investment decisions.

If you are a distribution network business, and you are trying to understand how different tariff designs can drive different customer and asset behaviour, then modelling like this can help you run “virtual tariff trials” up front, and can also be used to track and report on the actual technical and commercial performance of batteries that are on these tariffs.

If we can help, then hit us up.

Alex Leemon